Seller Financing: A Complete Guide for Buyers and Sellers

Seller Financing is a Real Estate arrangement where the property seller acts as the lender, helping the buyer directly instead of a traditional bank. This helps buyers bypass conventional mortgage processes, often benefiting those with limited down payment funds. It involves a promissory note and a deed of trust.

Maria Thompson

Generally, buying a property or business means applying for a bank loan, completing lengthy paperwork and waiting for approval. But what will happen when traditional financing is not available? In such a situation, Seller Financing can provide a practical alternative, allowing buyers and sellers to agree on payment terms directly without relying on a bank.

For many buyers and sellers, it creates opportunities that traditional loans may not provide. Buyers may find it easier to secure a deal, while sellers can attract more potential buyers and earn interest in payments. In this blog, you will learn about what is Seller Financing, its important terms, how it works and more. Let’s begin!

What is Seller Financing?

Seller Financing refers to an arrangement where the buyer is offered a loan from the seller to help them complete a purchase. Instead of relying on a bank, the buyer repays the seller through regular instalments over an agreed period. This approach is commonly used in business sales, where the seller may finance part or even the entire purchase price.

Seller Financing can make a deal more accessible by reducing the buyer’s need for a large bank loan. Also, it can benefit sellers by attracting more potential buyers, while enabling them to set up payment terms and maintain greater control over the entire transaction.

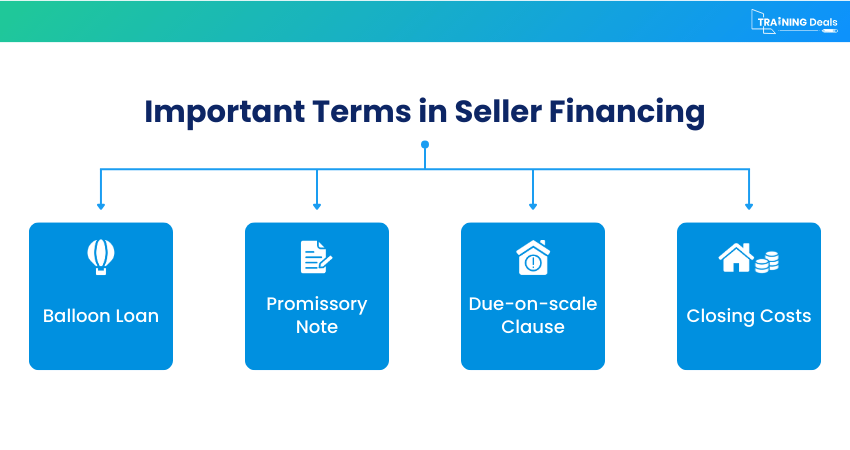

Important Terms of Seller Financing

Understanding the key terms in Seller Financing helps both buyers and sellers clearly define the agreement and avoid confusion during the transaction. Let’s look at the important terms below:

1) Balloon Loan: It is a loan that is not fully repaid during its set term. At the end of the agreement, the buyer must make a large final payment to clear the remaining balance.

2) Promissory Note: It’s a legal document outlining the terms and conditions of the financing agreement. It specifies details, such as the loan amount, repayment schedule, interest rate, and responsibilities of both the buyer and seller.

3) Due-on-sale Clause: It is a provision that needs the borrower to repay the remaining loan balance in full if the property or asset is sold before the loan is paid.

4) Closing Costs: It is the fees paid at the end of the transaction by the buyer, seller, or both. These may include commissions, taxes, title charges and record filing fees related to completing the sale.

How Seller Financing Works?

Seller Financing enables the seller to act as the lender, enabling the buyer to purchase a property or asset. Usually, the buyer pays a down payment and makes regular monthly payments to the seller until the agreed purchase price is fully paid. Let’s read more about it below:

1) Seller as the Primary Lender: The seller replaces a traditional mortgage, accepts a down payment, and receives monthly payments from the buyer until the purchase price is paid.

2) Co-ownership or Land Contract: In this arrangement, the buyer and seller share ownership. The buyer makes regular payments and gradually increases their ownership share, often completing with a balloon payment.

3) Junior Mortgage: If the buyer cannot secure enough financing from a bank, the seller may provide a second loan to cover the remaining amount. This bridges the gap between the buyer’s loan approval and the total purchase price.

4) Rent-to-own Agreement: Here, the buyer rents the property for a specific period while paying monthly rent. After the lease period ends, the buyer has the option to purchase the property, with part of the rent sometimes counted toward the sale price.

5) Assumable Mortgage: In some cases, the buyer may take over the seller’s existing mortgage, such as a Federal Housing Administration (FHA) loan. Then, continue making the payments under the same loan terms.

Seller Financing in Practice

Seller Financing lets the seller act as the lender, giving both parties flexibility to negotiate payments, down payments, and terms based on their needs. Let’s look at some of the key requirements below:

1) Asset Purchase Agreement: A legal contract outlining the sale terms and any seller-financing arrangements.

2) Personal Guarantee: Ensures the buyer is responsible for repayment, giving the seller recourse if payments are missed.

Also, some common conditions here include:

1) Loan Amount: Commonly 5% to 60% of the sale price, though some sellers may finance more with a larger down payment.

2) Down Payment: Usually around 10%, but negotiable.

3) Term Length: Typically, five to seven years, depending on agreement.

4) Interest Rate: Often 6% to 10% per year, depending on risk and negotiation.

These figures represent average ranges, not fixed rules. Terms negotiated between buyer and seller can vary widely depending on the property, market, and party's circumstances.

Keep your accounts accurate and smart with the Book Keeping Course – Join now!

Pros and Cons of Seller Financing

Both buyers and sellers can gain from Seller Financing, but it also carries certain risks. Understanding the advantages and disadvantages helps both parties decide whether this financing option suits their needs. Let’s look at them below:

1) Pros for Buyers

1) Alternative Finance: Seller Financing provides an option for buyers who cannot secure a traditional mortgage from financial institutions.

2) Quicker Purchases: Transactions can be completed faster because of less paperwork and no lengthy loan approval process from lenders.

3) Flexible Terms: Buyers and sellers can negotiate payment schedules, interest rates, and other conditions to suit both parties.

4) Lower Closing Costs: Seller Financing may reduce certain bank-related fees, making the closing process affordable.

2) Cons for Buyers

1) Higher Interest Rates: Interest rates in Seller Financing agreements may sometimes be higher than those offered by banks.

2) Risk of Default: In case the buyer fails to meet the terms of repayment, they may lose the property and the payments already made.

3) Due-on-Sale Clause: In case the seller has an existing mortgage, the lender may demand full repayment when the property is sold.

4) Balloon Payments: Some agreements require a large payment at a certain point during the loan term.

Learn how to build powerful financial spreadsheets with the Excel for Accounting Course now!

3) Pros for Sellers

1) Faster Sales: Seller Financing can speed up the sales process by attracting buyers who may not qualify for traditional loans.

2) Regular Income: Sellers receive steady income through monthly payments without managing the property.

3) Sell As-is: Properties can be sold without completing repairs that traditional lenders might require.

4) Investment Potential: Interest payments can provide a better return than investing the sale proceeds elsewhere.

5) Broader Buyer Pool: Offering financing can attract more potential buyers, increasing the chances of completing the sale.

4) Cons for Sellers

1) Payment Management: Sellers must monitor and manage the buyer’s payments throughout the loan term.

2) Credit Risk: Sellers need to carefully evaluate the buyer’s financial reliability before agreeing to the arrangement.

3) Default Risk: If the buyer stops making payments, the seller may need to repossess the property through legal processes.

4) Existing Mortgage Obligations: If the seller has a mortgage on the property, they may not receive upfront funds to fully repay it.

Advance your property finance expertise with the CeMAP Course (Level 1,2 and 3) - Sign up today!

Alternatives to Seller Financing

If Seller Financing is not a suitable option for your financing needs, several other financing methods may better suit your financial situation. In fact, the global Alternative Lending Platform Market is projected to reach £10.83 billion by 2030, reflecting the rapid growth of non-bank financing options worldwide. Let’s look at some alternatives below:

1) Conventional Mortgages: These are standard home loans provided by banks, building societies, and other lenders. The buyer borrows money from the lender and repays it over time with interest.

2) Joint Mortgages: Here, if a buyer finds it difficult to qualify for a mortgage independently. They may apply with a guarantor or a joint borrower who shares responsibility for the loan.

The correct financing option depends on your financial situation, credit profile and long-term goals. These alternatives can help you secure financing when Seller Financing may not be the most suitable option.

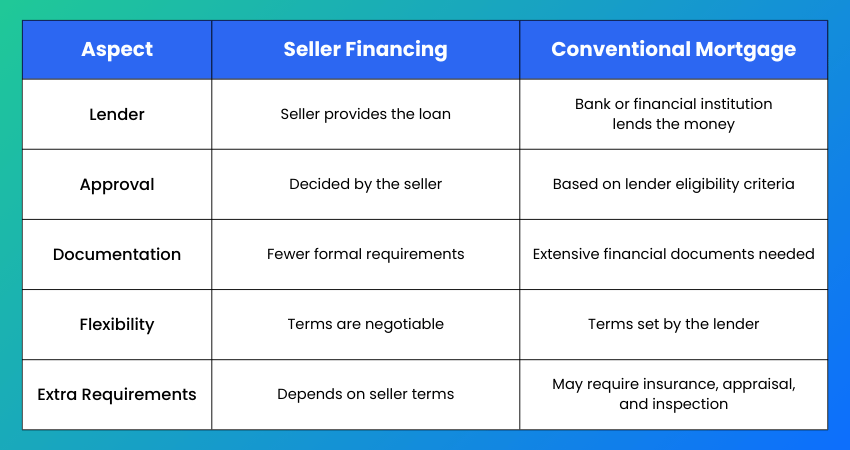

How is Seller Financing Different From a Conventional Mortgage?

Seller Financing and conventional mortgages are two ways to fund a property purchase. While both allow buyers to pay overtime, they differ in various ways. Let’s look at the table below:

With a conventional mortgage, buyers must meet the lender’s requirements, such as maintaining a suitable credit score and providing financial documents. They also need to pay various closing costs before the purchase is finalised.

In contrast, in Seller Financing, the seller acts as the lender and decides the financing terms. Here, the down payment, interest rate and repayment schedule are negotiated between the seller and buyer. This makes the process more flexible than traditional mortgage financing.

Conclusion

Seller Financing offers a flexible way to complete a property purchase when traditional loans are not suitable. Allowing buyers and sellers to agree on terms directly can make transactions quicker and more accessible, provided the agreement is carefully structured and clearly defined.

Build a solid Accounting expertise with Accounting Courses now!

Search

Latest Blog

What is Risk Mitigation: Types, Steps, and Best Practices

June 27, 2026The 5 Project Management Phases Every Professional Should Know

June 23, 2026Program Manager vs Project Manager: A Complete Comparison Guide

June 23, 2026Project Charter Explained: Components & How to Write It Effectively

June 23, 2026FAQ

No FAQs available for this blog.